Woori Bank implements measures to streamline household debt

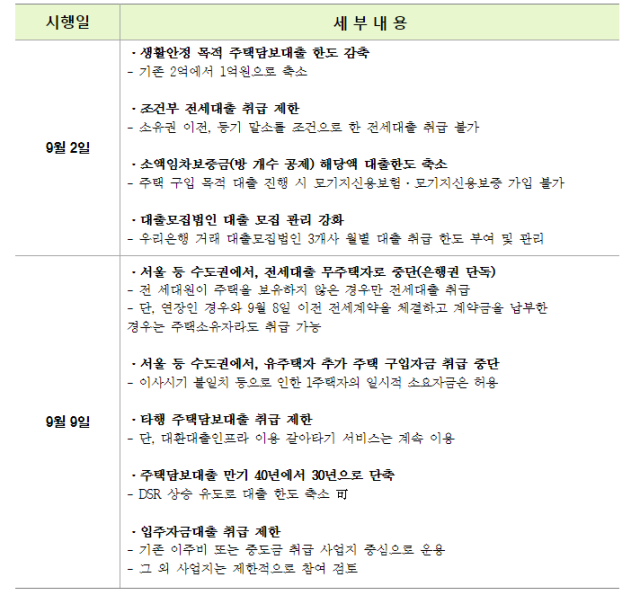

No loans for additional home purchases in the Greater Seoul area for primary homeowners

For lease loans, all household members must be non-homeowners

Maximum loan term for housing loans reduced from 40 years to 30 years,

Woori Bank headquarters. Photo provided by Woori Bank,

, ‘[Seoul Economy]’,

,

, ‘Woori Bank has decided not to provide loans for the purpose of purchasing additional homes in the Seoul metropolitan area for individuals who own at least one home starting from the 9th of this month. Lease loans for primary homeowners will also be completely suspended. This is part of the bank’s intention to curb speculative demand such as gap investments and focus on managing household debt based on actual demand.’,

,

, ‘Woori Bank announced on the 1st that it will implement the ‘Household Debt Efficiency Plan Centered on Actual Demand’ starting this month.’,

,

, ‘According to the efficiency plan, Woori Bank will not provide loans for primary homeowners who own at least one home in Seoul or the surrounding metropolitan area to purchase additional homes starting from the 9th. However, conditions allowing existing home sales due to relocation discrepancies will be permitted, and funding for non-homeowners will continue to be supported without interruption to minimize the disadvantages for actual demand customers.’,

,

, ‘Lease loans will only be provided to non-homeowners. This is limited to cases where all household members do not own a home to block speculative demand such as gap investments. However, in cases of lease extensions and agreements signed before the 8th with earnest money paid, the bank plans to provide lease loans even to homeowners to minimize confusion.’,

,

, ‘The maximum term for housing loans is reduced from the existing 40 years to 30 years. This is a plan to induce an increase in the Debt Service Ratio (DSR) to borrow within the range that can be repaid based on income, naturally reducing the borrower’s loan limit. If the DSR increases, for example, if a borrower with an annual income of 50 million won takes out a loan at an interest rate of 4.5%, the loan limit will decrease from 370 million won to 325 million won, a reduction of 45 million won, or about 12%. In addition, the bank will restrict in-person loan changes at bank counters and continue to allow switching services only through online loan changes.’,

,

, ‘Apartment occupancy loans will be operated mainly on a project-by-project basis that Woori Bank dealt with for moving expenses or down payments, with limited participation in other projects. This is to restrain excessive inter-bank competition and ensure that only necessary funds flow to consumers.’,

,

, ‘Starting from the 2nd, the loan limit for living stability loans secured against homes will be reduced from 200 million won to 100 million won. Moreover, the bank plans to actively curb household loans by △ restricting lease loans based on conditions such as ownership transfer and registration cancellation △ limiting the monthly handling limit for loan solicitors △ reducing the loan limit for modest rent guarantees (deducted by the number of rooms) for MCI·MCG housing collateral loans.’,

,

, ‘A Woori Bank official stated, “As the trend of increasing household debt continues, we have decided to implement loan management measures to prevent speculative demand.” They also said, “However, we will continue to supply to non-homeowners and the general public to maintain the efficiency of overall household loan operations.”‘,

,

,

Photo provided by Woori Bank,

,

,