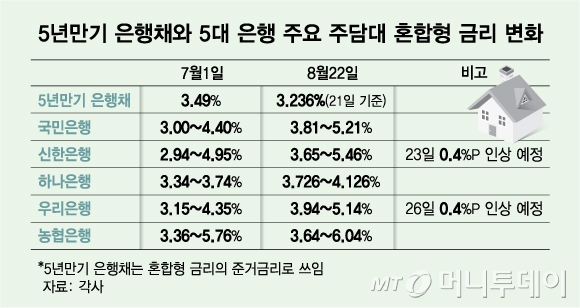

Changes in 5-year bank bond and 5 major bank composite interest rates / Graphic = Kim Dana, ‘While the Bank of Korea decided to maintain the base interest rate, interest rates for bank mortgage loans are rising. The interest rates that borrowers are currently feeling have surpassed 4%. Some banks have raised interest rates by more than 1 percentage point (P) in the past month.’,

,

, ‘According to financial sources on the 22nd, the composite interest rates (5-year fixed, 5-year interval) of KB Kookmin, Shinhan, Hana, Woori, NH Nonghyup, and other 5 major banks were in the range of 3.65% to 6.04% for the day. Compared to last month (2.94% to 5.76%), the lower end of the interest rates increased by 0.71 percentage point (P) and the upper end by 0.28% P.’,

,

, ‘Although the Bank of Korea’s Monetary Policy Board decided to maintain the base interest rate at 3.5% and the number of board members forecasting a base interest rate cut within the next 3 months increased from 2 to 4, composite interest rates are expected to rise further. Shinhan and Woori banks plan to increase their composite interest rates by 0.4% on the 23rd and 26th, respectively.’,

,

, ‘Since last month, bank composite interest rates have been rising contrary to market trends. While the interest rate on 5-year bank bonds, which serves as the reference rate for composite interest rates, fell from 3.49% in early last month to 3.236% the day before, composite interest rates increased. Banks have collectively raised interest rates in line with financial authorities’ goals of managing household debt. Some banks have raised interest rates by more than 1% P in the past month.’,

,

, ‘The average composite interest rates newly handled by the 5 major banks in June ranged from 3.60% to 3.83%, but the actual composite interest rates perceived by general borrowers have effectively exceeded the 4% threshold. Banks calculate composite interest rates by adding a margin to the reference interest rate and then deducting individual preferential rates.’,

,

, ‘To obtain a loan at interest rates of 3.64% to 3.94% with maximum preferential rates, it is not easy for general borrowers to meet the criteria. For example, in the case of Kookmin Bank, considering that the preferential rate for vulnerable borrowers such as basic livelihood recipients and disabled customers is 0.3% P, general customers start with an interest rate of around 4.11%. If Shinhan and Woori banks proceed with the planned rate hikes, the lower end of the interest rates would exceed 4%.’,

,

, ‘As increasing interest rates alone cannot curb the demand for household loans, authorities and banks are also reducing loan limits. Financial authorities have announced plans to implement the Debt Service Ratio (DSR) 2nd stage as scheduled from September, and have further reduced bank loan limits by raising the margin interest rates for buying houses in the Seoul metropolitan area. A borrower with an annual income of 50 million won seeking a 30-year adjustable rate loan (rate 4.5%) in the Seoul metropolitan area would see their limit reduced from 315 million won to 287 million won.’,

,

, ‘Banks are also individually reducing loan limits. Shinhan Bank announced that it would halt the processing of Mortgage Credit Insurance Plus (MCI, MCG) loans from the 26th. With the cessation of MCI (Mortgage Credit Insurance) and MCG (Mortgage Credit Guarantee), it is expected that there will be a reduction in loan limits for Seoul apartments worth more than 55 million won. Following Kookmin Bank’s suspension of the multiple homebuyer composite interest rates, Shinhan Bank has decided to discontinue the conditional lease loans that can be used for gap investment.’,

,

, ‘A banking industry official stated, “Most of the rate discounts that can be offered at the branch level have been blocked,” adding, “As financial authorities have requested measures to reduce loan limits in addition to raising interest rates, it is expected that the loan threshold will become even higher.”‘,

, ‘article_split’,

,

,