Obtained the Cubten Audit Report

Coupang was in a state of complete capital erosion at the time of acquisition

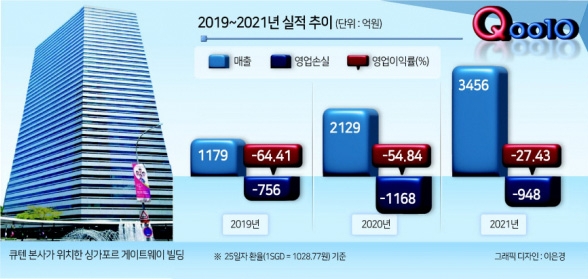

Cubten’s operating profit margin is a serious -27.43%,

,

,

, ‘A tremendous insolvency of Singapore-based Cubten, which is at the peak of TMON and WeMakePrice’s delayed settlement crisis, has been revealed. It was confirmed that at the time of acquiring TMON, Cubten suffered an annual deficit of 100 billion won.’,

,

, ‘At that time, TMON was in a situation where liabilities were higher than assets, in a state of complete capital erosion, and it means that a loss-making company forcibly acquired a loss-making company. ▶Related articles on pages 2,3,4’,

,

, ‘This is the first time that Cubten’s specific performance has been disclosed. It is seen as a move by Cubten, which was running deficits, to take over a poorly performing company in a rush for a Nasdaq listing.’,

,

, ‘According to the financial results for the previous year (2021) obtained exclusively by this newspaper on the day of the acquisition of TMON by Cubten, Cubten’s deficit amounted to 948 billion won in a year (converted to KRW standard). The operating profit margin was also a serious -27.43%.’,

,

, ‘In 2019 and 2020, operating losses amounted to 756 billion won and 1168 billion won, respectively. This means that deficits accumulated every year until just before the acquisition of TMON in 2022.’,

,

, ‘In the meantime, sales increased from 117.9 billion won to 345.6 billion won. It was a situation where only the appearance was expanded without substance. As a result, the cumulative loss of Cubten until the year before the acquisition of TMON was revealed to be 429.9 billion won.’,

,

, ‘At the time of acquiring TMON, TMON was in a serious state of capital erosion. However, Cubten, which acquired it, was already suffering from deficits.’,

,

, ‘The problem is that these circumstances were not known at the time of the acquisition. Cubten’s basic acquisition approach and investment size were only speculated due to lack of information.’,

,

, ‘Considering Cubten’s deficit situation at that time, the acquisition of TMON through stake exchange is interpreted as virtually the only acquisition option.’,

,

, ‘The lack of proper disclosure of Cubten’s financial situation was partly due to the trust in Gu Young-bae, CEO of Cubten. Gu, the founder of Gmarket, the first open market in Korea, is also known as the “father of 1st generation e-commerce.” After selling Gmarket to eBay in 2009, he moved to Singapore under a non-competition clause for 10 years and started the Cubten business.’,

,

, ‘Little information was known about Cubten based in Singapore other than being founded by Gu. However, due to Gu’s legendary reputation, there was more anticipation than suspicion when he acquired TMON.’,

,

, ‘The tarnishing of Gu’s reputation began with the rapid acquisitions of Interpark E-commerce, WeMakePrice, WISH, AK Mall, and others following TMON. Concerns arose as they embarked on a rapid expansion towards a Nasdaq listing through large-scale acquisitions in a short period of time.’,

,

, ‘As the companies they acquired struggled with losses without recovering, it eventually led to a large-scale settlement delay crisis for TMON and WeMakePrice.’,

,

, ‘Partner companies selling products through TMON, WeMakePrice, Interpark, and other Cubten group affiliates amount to as many as 60,000. The annual transaction amount of these three companies reached 6.9 trillion won based on last year. The extent of the damage caused by the settlement delay crisis is currently difficult to estimate.’,

,

, ‘An industry official stated, “There are doubts about whether the Cubten group has the cash liquidity to resolve this crisis.”‘,

,

, ‘Meanwhile, Ryu Hwahyun, co-CEO of WeMakePrice, stated regarding the settlement delay crisis, “We will make sufficient preparations for consumer refund funds to prevent any damages,” and said, “The unsettled amounts that need to be returned to sellers by merging TMON and WeMakePrice are being secured by Cubten.” Kim Sang-soo, Reporter’,

,

,