Impact of no large-scale sales like Hanwha Ocean

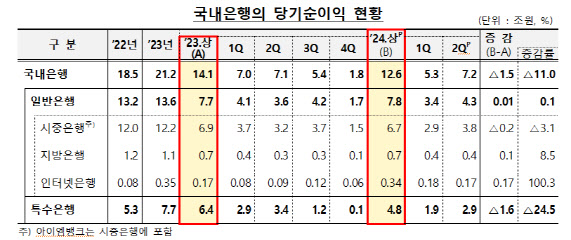

ROA 0.67% · ROE 9.03%, ‘[E-Daily Song Ju-o Reporter] In the first half of this year, the net profit of domestic banks decreased by 11.0% (1 trillion 500 billion won) compared to the same period last year, reaching 12 trillion 600 billion won. Financial authorities analyzed that last year, the net profit of the Industrial Bank greatly increased due to the sale of Hanwha Ocean in the first half of the year, but this year, there was no such large-scale sale.’,

,

,

|

, ‘The Financial Supervisory Service announced the ‘First Half of 2024 Domestic Bank Operating Performance (Estimated)’ on the 22nd. Specifically, looking at it, the net profit of commercial banks totaled 6 trillion 700 billion won, a decrease of 200 billion won. On the other hand, internet banks and regional banks increased by 170 billion won and 100 billion won, respectively. The net profit of special banks amounted to 4 trillion 800 billion won, a sharp drop of 1 trillion 600 billion won. Special banks had a sharp increase in net profit last year due to the sale of Hanwha Ocean by the Industrial Bank. This year, it decreased without large-scale sales.’,

,

, ‘The return on assets (ROA) of domestic banks in the same period was 0.67%, down 0.12 percentage points from the previous year (0.79%). The return on equity (ROE) was 9.03%, a decrease of 1.82 percentage points from the previous year (10.85%).’,

,

, ‘During the same period, interest income reached 29 trillion 800 billion won, an increase of 400 billion won compared to the same period last year. The increase in interest-earning assets (4.1%) played a major role. Due to a narrowing of net interest margin (NIM) (△0.06 percentage points), the growth in interest income slowed down. Non-interest income decreased by 400 billion won compared to the same period last year, totaling 3 trillion 400 billion won. Fee income and securities-related income each increased by 200 billion won, while foreign exchange and derivative-related income decreased by 600 billion won.’,

,

, ‘Selling and administrative expenses of domestic banks increased by 300 billion won to 12 trillion 800 billion won. Labor and material costs increased by 200 billion won and 100 billion won, respectively.’,

,

, ‘The provision for credit losses of domestic banks decreased by 500 billion won to 2 trillion 600 billion won. This was mainly due to the base effect caused by the significant increase in credit loss expenses of domestic banks last year following improvements in the methodology for calculating loan loss provisions, among other factors.’,

,

, ‘Non-operating losses decreased sharply by 2 trillion 300 billion won to 1 trillion 400 billion won compared to last year. It is analyzed that non-operating income decreased due to the provision for equity-linked securities (ELS) (1 trillion 400 billion won) made in the first half of this year.’,

,

, ‘A spokesperson from the Financial Supervisory Service said, “There is a possibility that financial market volatility may increase due to uncertainties in major countries’ monetary policies and geopolitical risks, so we plan to continue to induce sufficient loss-absorbing capacity enhancements to ensure that banks can faithfully perform their fundamental function of fund intermediation even in times of crisis.”‘,

,

,